Stablecoin Yields vs Singapore Savings Accounts: A 2026 Risk-Return Comparison

Why Singapore savings rates are no longer competitive

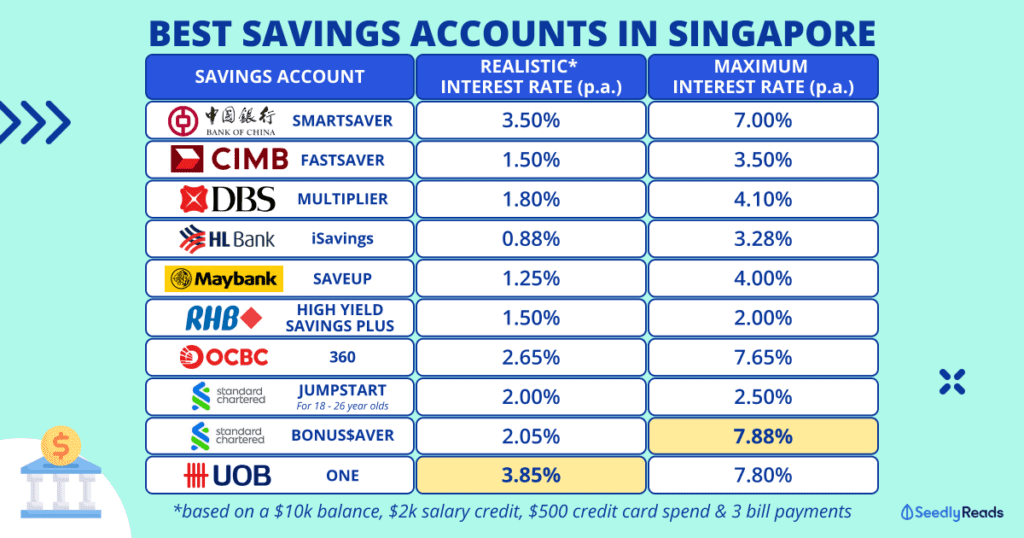

A few years ago, parking cash in a Singapore savings account felt like a no-brainer. Post-pandemic rate hikes pushed yields to 3–4% on accounts like UOB One and OCBC 360 — genuinely useful returns without touching your investment portfolio.

Bank Interest Rates in March 2024

That era is over.

High-yield savings accounts in Singapore aren't as high-yield as they used to be. Both UOB One and OCBC 360 cut their rates last year — UOB One now sits at up to 1.90% p.a., while OCBC 360 offers up to 2.45% p.a., and CIMB, which was my favourite no-frills savings account, now only boast a 0.5% p.a. or up to 2.30% p.a. if you fulfil the other requirements like salary credit, spend and incremental balance. Missing one of those means you only get the prevailing interest rate.

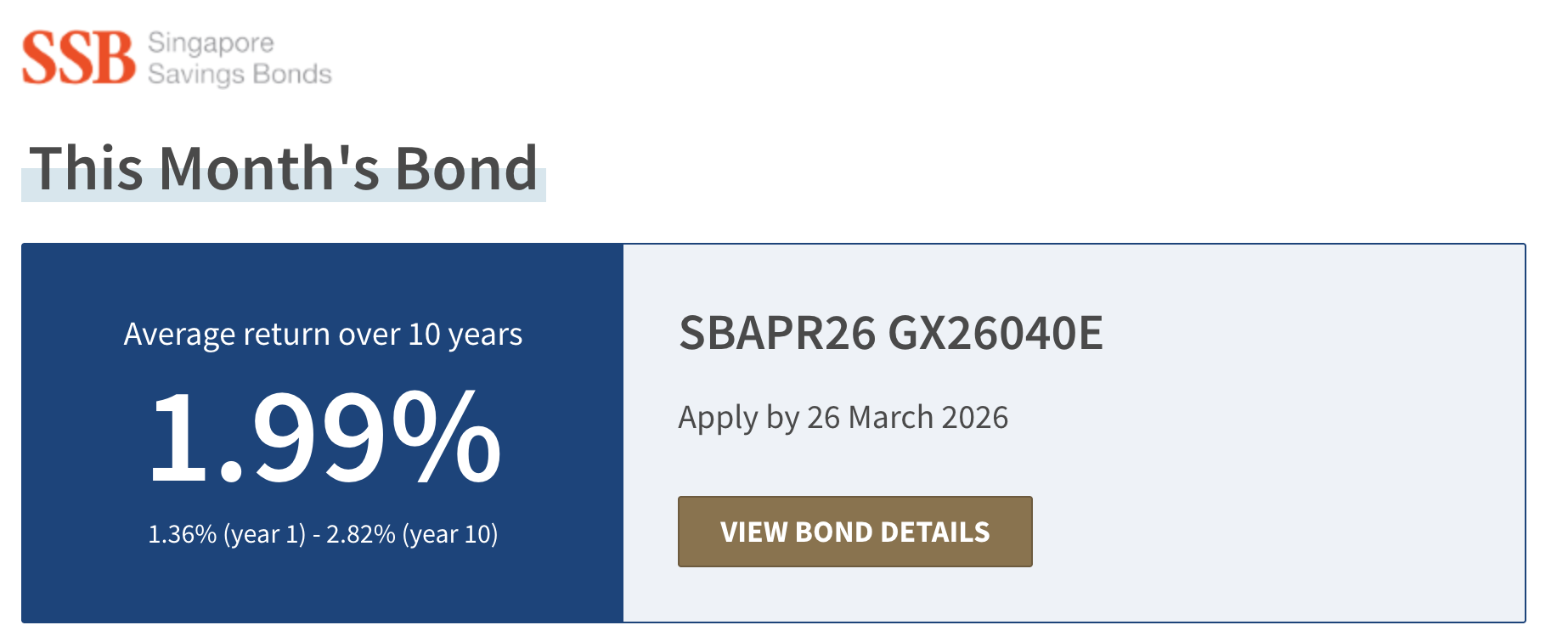

The latest Singapore Savings Bonds for February 2026 offered average returns of 1.99% p.a. — only if you hold for the entire 10 years. For cash that needs to stay liquid, the traditional toolkit is increasingly inadequate.

Feburary 2026 SSB Issuance, giving only 1.99% returns.

How stablecoin yields actually work

Before comparing numbers, you need to understand what you're actually doing when you "earn yield" on a stablecoin — because it's fundamentally different from a savings account. And it’s really different!

What is a stablecoin?

A stablecoin is a cryptocurrency pegged 1:1 to a fiat currency, usually the US dollar. USDC and USDT are the two largest. Think of it as a digital dollar that doesn't move in price. 1 USDC = 1 USD — always (in theory).

Different types of stablecoins | Credit: https://bfaglobal.com/insights/could-stablecoins-disrupt-instant-payment-schemes/

Where does the yield come from?

There are a few mechanisms, and they carry very different risk profiles:

Treasury-backed yield — Stablecoin issuers like Circle (USDC) hold reserves in US Treasury bills. Platforms pass some of that yield back to users as a "rewards" product. This is the lowest-risk form — you're essentially getting indirect T-bill exposure.

Lending yield (DeFi) — Protocols like Aave and Compound automatically match lenders and borrowers on-chain via smart contracts. You deposit stablecoins, borrowers pay interest, and you receive a share. Rates are variable and determined algorithmically based on pool utilisation: when most deposited stablecoins are being borrowed, rates are high; when borrowing demand is low, rates drop. Smart contract risk is the main concern.

Lending yield (CeFi) — Platforms lend your stablecoins to institutional borrowers, who post crypto collateral. You earn the interest. The risk here is the platform itself — if it goes under (think Celsius, Voyager), your funds can be at risk.

The key takeaway: yield source = risk source. Higher yield almost always means more counterparty, platform, or smart contract exposure.

Supplying USDC on AAVE gives you a 1.84% APY!

The real comparison: Chocolate Finance, Tiger Vault, and DeFi yields

Let's get concrete. Here are many options available to Singaporeans today. But I’ll be covering those that I’m using.

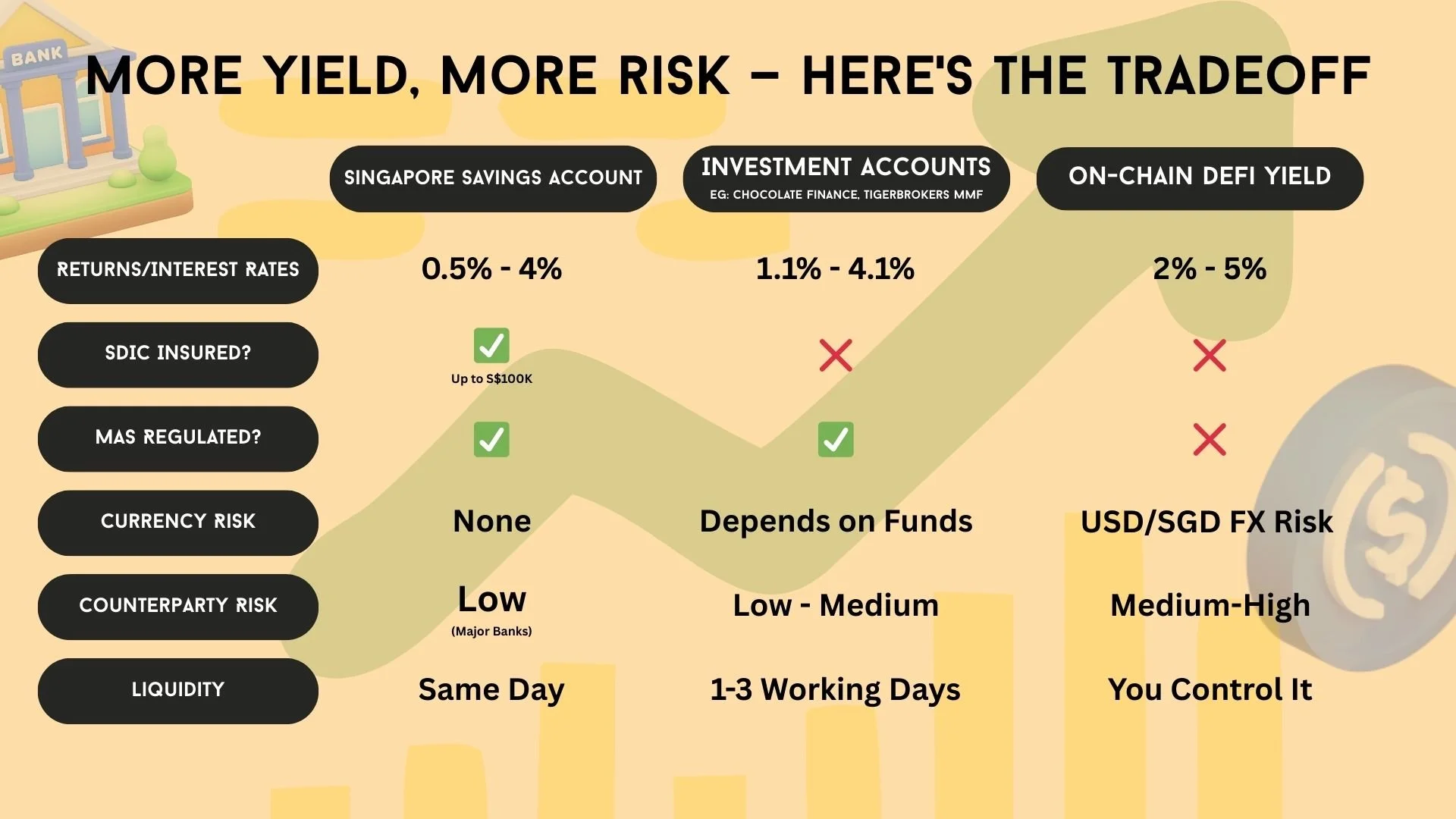

Risk vs Reward for different savings accounts vs investment products

Chocolate Finance (SGD & USD)

Chocolate Finance is an MAS-regulated fund manager (CMS101452) that invests your cash into short-term, investment-grade bond funds managed by names like Fullerton, Lion Global, and Aberdeen. You see daily returns in-app. No lock-in.

Current rates* (as of early 2026):

SGD: 2% p.a. on the first S$20,000, 1.8% p.a. on the next S$30,000

USD: 4.1% p.a. on the first US$20,000, 3.8% p.a. on the next US$30,000

*Rates are accurate at the time of writing

The rates are supported by their Top-Up Programme — if the portfolio underperforms on balances up to S$50k and US$50k, Chocolate tops up the difference until 30 June 2026, or until they hit S$1.5 billion AUM, whichever comes first.

Key risks to know:

Returns are not guaranteed, and foreign currency deposits are not covered by SDIC. Unlike SGD bank deposits, your funds are separately custodised and remain withdrawable, but this is not a bank deposit.

USD account adds FX risk — if the dollar weakens against SGD, your effective return in SGD terms shrinks.

Withdrawals are not instant, usually T+3 or less.

Best for: Singaporeans who want a no-fuss, app-based yield product with MAS-regulated infrastructure. SGD option for your main cash stack. USD option if you're already USD-denominated or comfortable with the FX play.

Sign up here to take advantage of the Chocolate Top-Up Program! I personally use Chocolate Finance too!

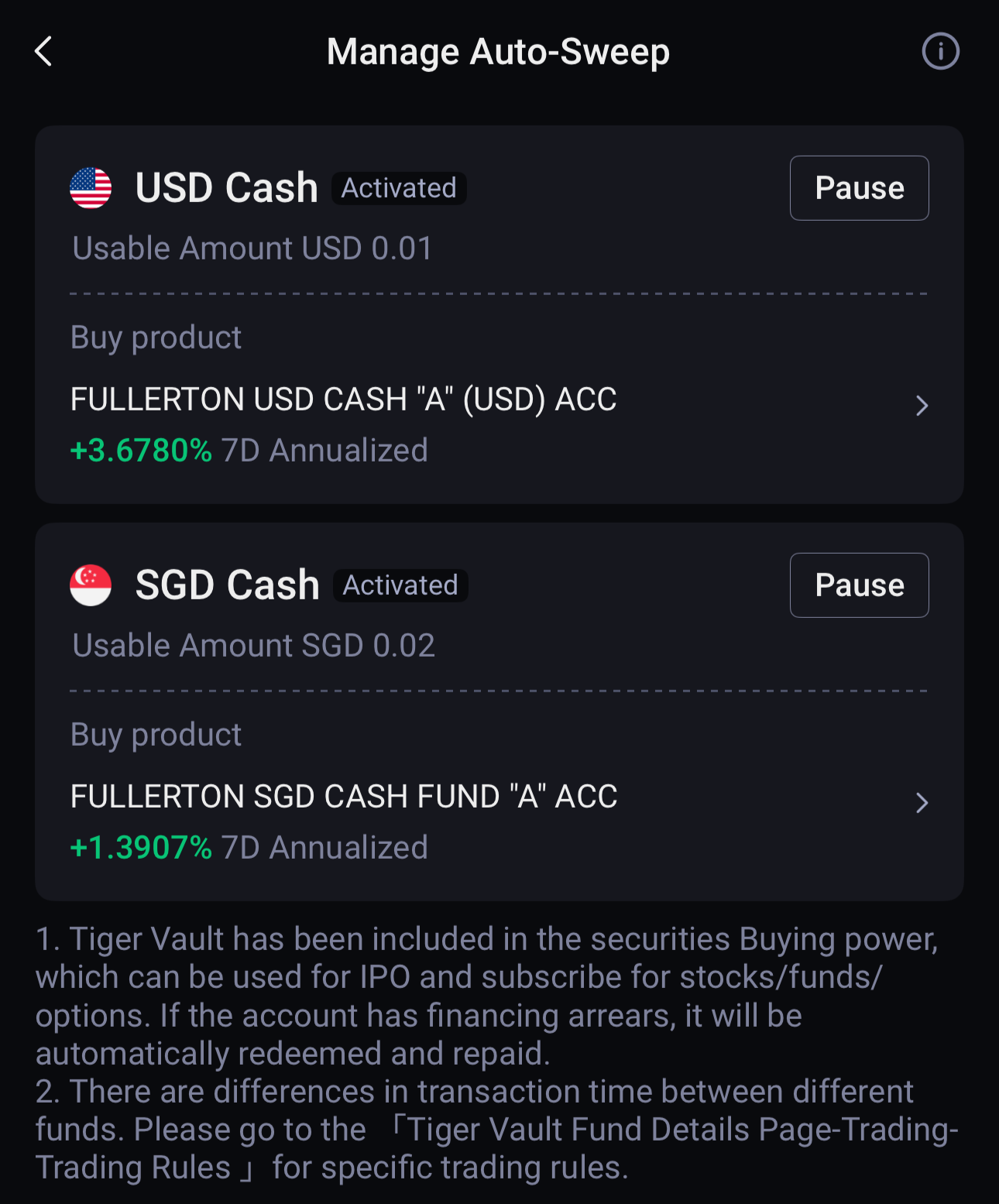

Tiger Vault (Money Market Fund via Tiger Brokers)

Tiger Vault is Tiger Brokers' cash management feature, which automatically sweeps your idle brokerage cash into money market funds via their Auto-Sweep function — no manual action needed once activated.

Tiger Vault offers access to several funds, with the Fullerton SGD Cash Fund being one of the most widely recommended for its large fund size, low expense ratio, and consistent yield among Singapore money market funds.

Current yields: Tiger Vault yields approximately 1.5–2.0% on SGD idle cash. USD funds have typically higher returns depending on market conditions.

TigerBrokers USD and SGD MMF Rates

Why use Tiger Vault?

The real value proposition isn't the yield — it's the idle cash efficiency. If you're already a Tiger Brokers investor, your uninvested cash earns something while waiting for your next trade, and it automatically converts to buying power when you execute. It's the best way to ensure your "war chest" isn't sitting dead.

Key risks:

MMFs are investment products, not bank deposits. Your capital is not guaranteed — while extremely rare under Singapore's MAS-regulated framework, an MMF can technically "break the buck" if NAV falls below S$1.00 per unit.

Withdrawals require 1 working day to process, plus another 1–3 business days for bank transfer.

Best for: Existing Tiger Brokers users who want their uninvested cash working harder without moving funds to a separate platform.

New to Tiger Brokers? Deposit US$1,000 and get US$150 in welcome rewards

DeFi Stablecoin Yields

This is the on-chain option — you connect a crypto wallet, deposit USDC or USDT directly into a protocol, and earn variable yield with no intermediary.

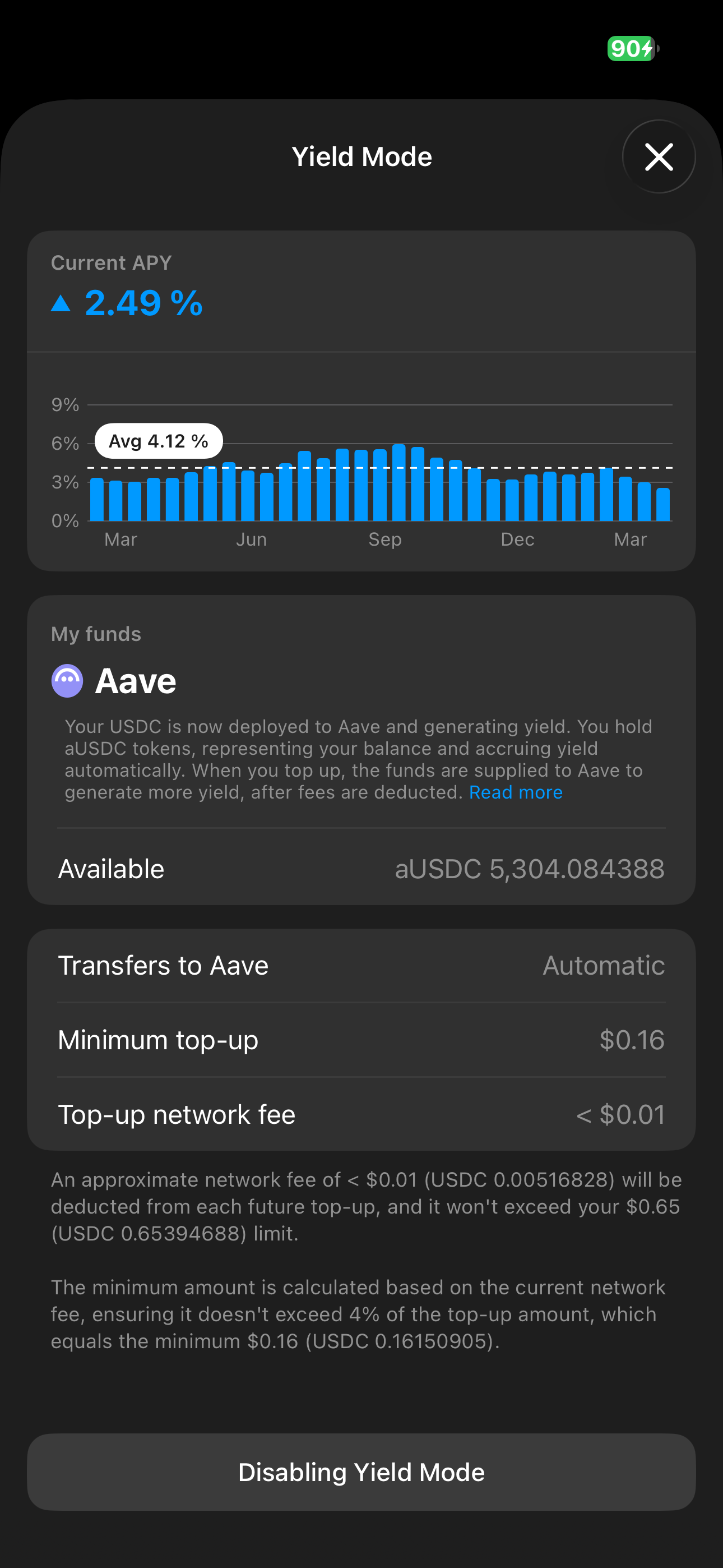

Aave is the leading option for flexible, self-custody DeFi yield with transparent, variable rates. When you supply USDC to Aave, you receive aUSDC — a receipt token that represents your deposit plus accrued interest.

AAVE USDC Yields on Tangem Wallet

Current yields: As of early 2026, DeFi protocols like Aave and Morpho offer rates similar to or slightly higher than high-yield savings accounts, typically in the 1–5% range depending on market utilisation. Rates fluctuate significantly — when borrowing demand is low (as it has been in the current macro environment), yields compress or decrease.

The honest tradeoff: DeFi Yields is best for users who value self-custody, transparency, and flexibility, and who can manage wallets safely. But the friction is real — you need a wallet, you need to bridge funds on-chain, you pay network gas fees, and there is no MAS safety net if something goes wrong.

For most Singaporeans, DeFi yield makes sense only if you're already crypto-native and can stomach the complexity. This is not a starting point. Don't start here.

Best for: Crypto-native users who already self-custody and want to put stablecoins to work without handing custody to a CeFi platform.

If you're going the DeFi route, a hardware wallet is non-negotiable. Get 10% off a Ledger | 10% off Tangem

Risk Framework: When do these tools & platforms make sense?

✅ Worth exploring if:

You have cash beyond your emergency fund (3–6 months of expenses)

You understand these are investment products — not bank deposits

You're using MAS-regulated platforms for the bulk of your allocation

For DeFi: you already self-custody and understand smart contract risk

❌ Probably not right if:

This money is your emergency buffer — Protection matters more than yield here

You're chasing high (10–15%) DeFi yields without understanding what drives them

You're converting SGD to USD purely for the rate difference without accounting for FX risk

You've never held crypto or a self-custody wallet before

Ready to put your idle cash to work?*

💸 Chocolate Finance — Daily returns with no lock-in!

📈 Tiger Brokers — US$150 welcome reward when you deposit US$1,000**

🔐 Going on-chain? Secure your crypto first — Get 10% off a Ledger | 10% off Tangem

*Some links above are affiliate links. You never pay extra, and it helps keep this content free.

** Rewards might change depending on ongoing promotions and campaigns