Is Chocolate Finance Safe? My 2026 Cash Strategy

We have seen interest rates fall since late 2025. And with the Red packet money that we have gotten from the Lunar New Year, we want to ensure that the money we got, can grow instead of diminishing as time goes by due to inflation.

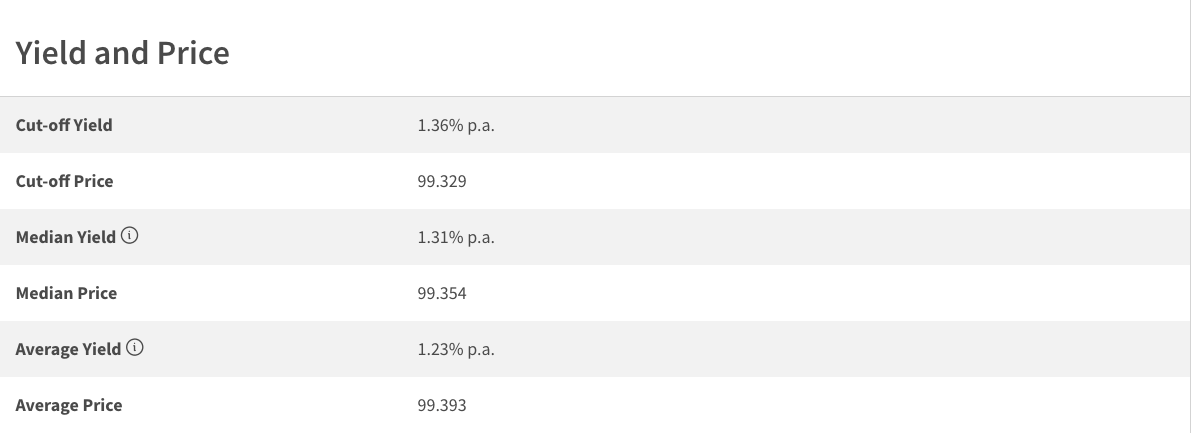

If we look at the T-bill interest rates, it gives me the shivers because just a year ago, the interest rates were 2-3%, but now they’re sitting at 1.36% for the latest issuance.

SSB February 2026 Cut-off Yield.

And this brings up the question of “Where’s the best place to put our idle money?”

Luckily for us, there are many different fintechs, neo-banks and banks in Singapore, which allow us to earn a return on our investments, which I have covered in past videos. But recently, I got in touch with the Chocolate Finance team, and this changed my mind a little.

As a disclaimer, Chocolate Finance did sponsor this video, but what I’ll be sharing is my own personal experience of using the application thus far.

As you guys know, I dabble with some stablecoins and also some high-yield savings accounts to maximise my money while we all work hard in our jobs and bring bread to the table.

We got high-yield savings accounts like OCBC 365, UOB ONE, and Trust Bank with their different plans. So while they all provide good interest, one of my biggest irks with them is the need to jump through hoops to get that high interest.

Why do I use Chocolate Finance?

Though I’m an avid user of the UOB ONE, I need to jump through hoops like crediting salary, do a minimum spend of $500 and based on my account balance, I’ll get a certain interest rate. But for the working class like us here, I believe what we want is the option that just makes our money work harder for us, not the other way round.

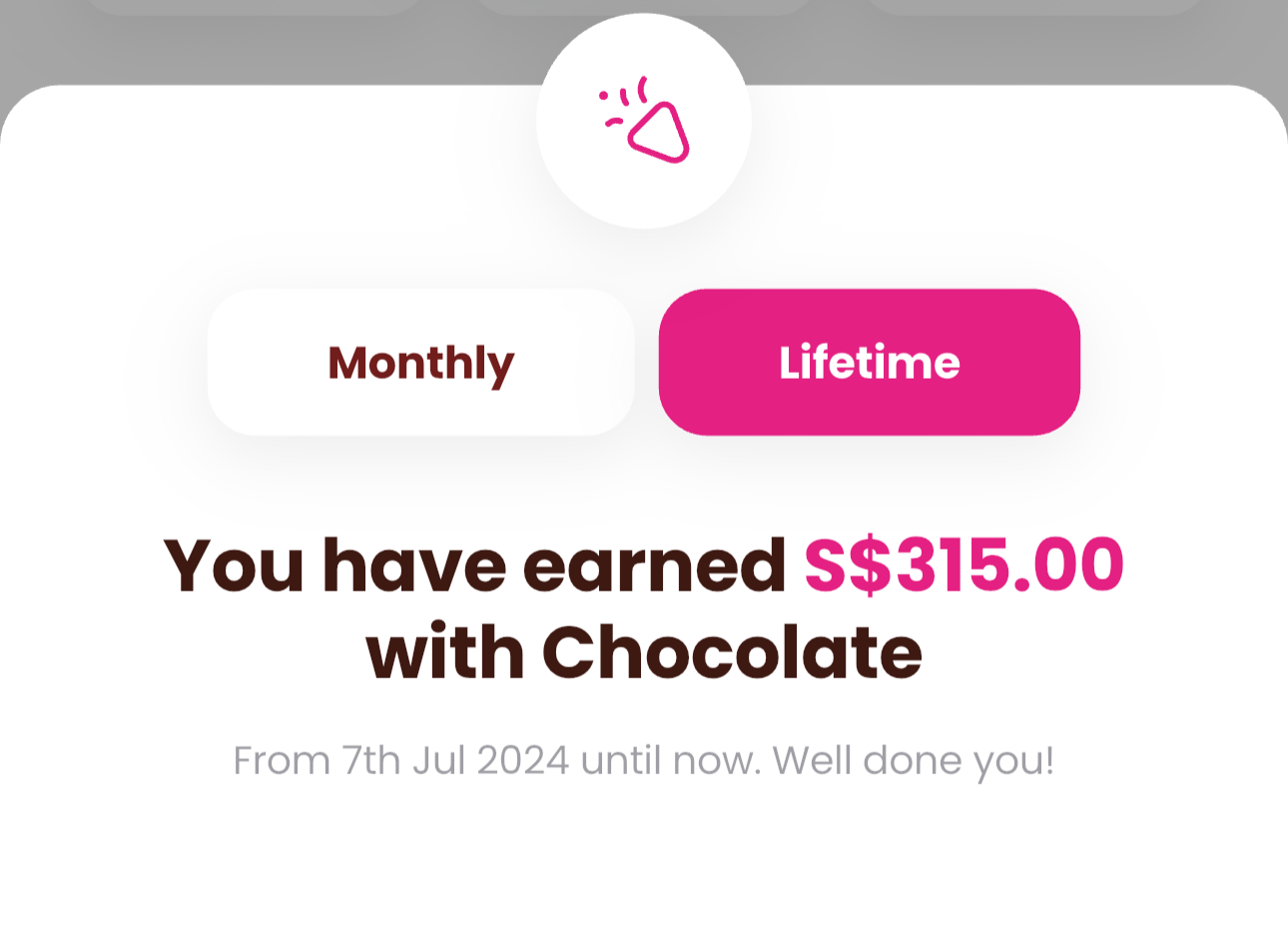

And this is where Chocolate Finance comes in. Once again, this is based on my own experience so far, and I’ll be honest, I have been using them for a while back in mid 2024, so my lifetime interest is $300+. But I stopped halfway through as I needed money to invest in my cafe, hence I moved some money out.

My lifetime earnings with Chocolate Finance

But I deposited money again in 2025 because I couldn’t find any better platforms that were providing better returns with no frills. And when I mean no frills, it means depositing money and not needing to do anything else.

How does Chocolate Finance work?

Let me take you through how it works real quick, so you get an idea of how no hoops it really is.

And if you haven’t gotten the app, I’ll leave my link in the description down below so you get the correct app and also show Chocolate Finance that I sent you to their platform!

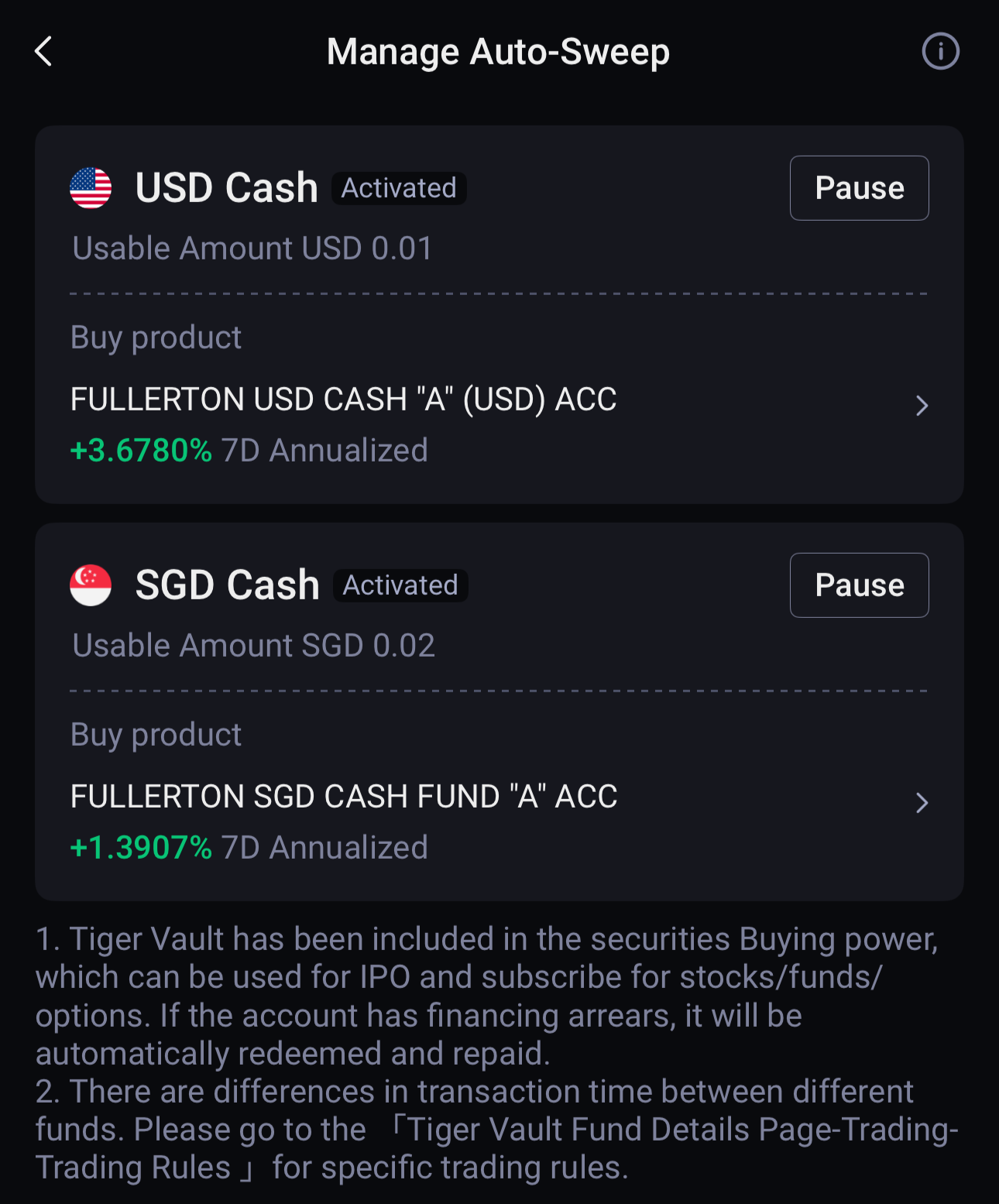

Once u got the app and finish the easy sign-up via SingPass, you will see a few things on the screen. You can deposit SGD or USD, and each currency has its own returns, 2% p.a. for the first S$20k and 1.8% p.a. for the next S$30k for SGD and 4.1% p.a. on the first US$20k and 3.8% p.a. on the next US$30k for USD.

Now the big question that most of you might have is, “Where do the returns come from?” For most banks or even DeFi protocols, it’s usually through a lending and borrowing system. For example, Money is lent out at 5%, the platform or bank takes a cut, and gives the remaining interest to the depositor, simple and straightforward.

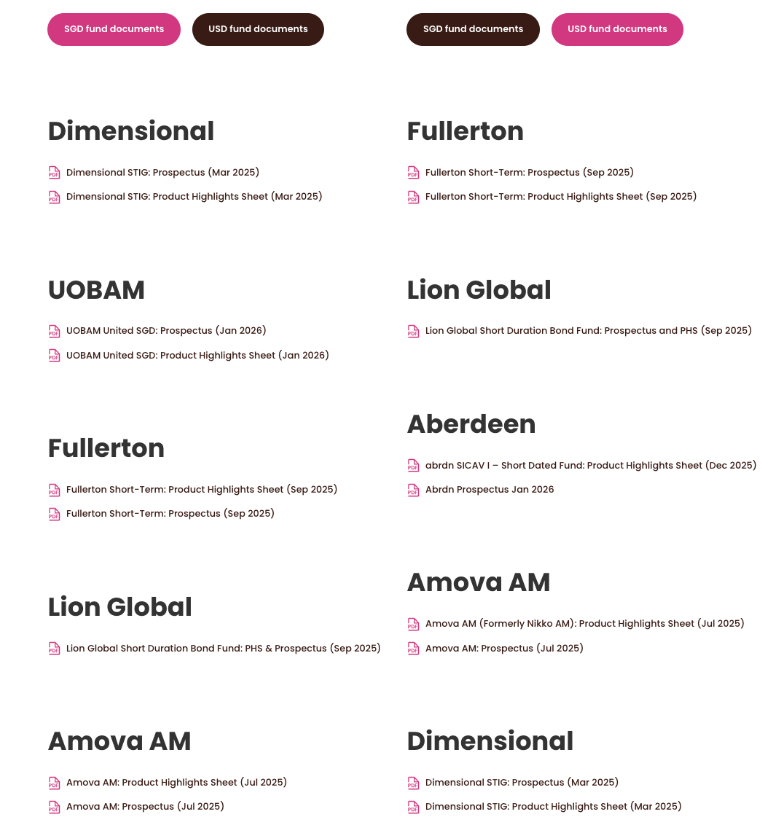

With Chocolate Finance, it works a little differently. When you deposit money into Chocolate Finance, your money is invested in a portfolio of funds which is curated and carefully selected to optimise risk-adjusted returns based on factors like duration, yield to maturity, credit quality and currency.

Funds that Chocolate Finance invests into based on currency

This allows the portfolio to deliver a return of 2% p.a. for the first S$20k and 1.8% p.a. for the next S$30k, and anything above is targeted at 1.8% p.a.. And what I like about this is that Chocolate Finance only takes a fee or makes money when they deliver those returns, which is stated.

And right now, the ‘Chocolate Top-Up Program’, which is an incentive program. This program is in place to support the returns for 2% p.a. on the first S$20k and 1.8% p.a. on the next S$30k. Similar to the USD, it’s 4.1% p.a, for the first US$20k and 3.8% p.a. for the next US$30k. This means if, for some reason, the portfolio underperforms, the difference will be topped up by Chocolate Finance, so we get to enjoy the current rates!

However, this has a Qualifying Period which runs from now till the 30th of June 2026 or until the Assets Under Management (AUM) reaches $1.5billion, whichever comes first, and Chocolate Finance holds the discretion to extend or remove the Top-Up Programme.

Chocolate Finance vs Brokers vs Banks

Now, let’s talk about other options and how they stack against Chocolate Finance and the different features that each of them has.

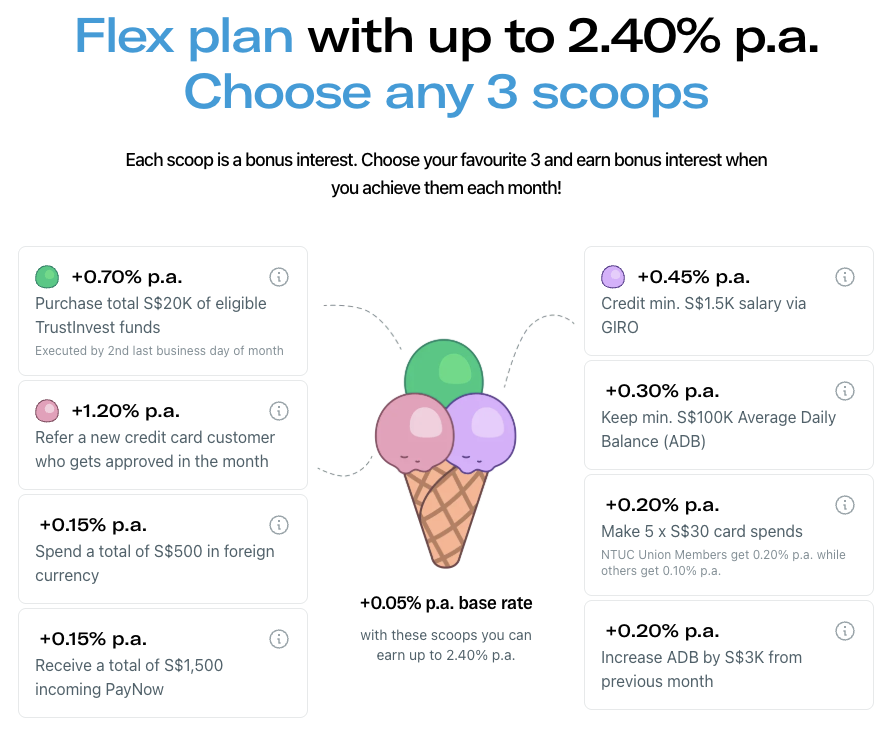

Starting with the banks, we know the high-yield savings accounts like UOB ONE, Mari Bank or even Trust Bank have some form of hoops to jump through. For quick reference, UOB ONE needs Salary Credit + $500 minimum spend, Maribank gives 2.85%, but you’ll need to deposit $5,000 to $20,000, Trust Bank have their different plans and even with the flexi plan, which I feel is the best, you’ll need to do spending, transfer and salary crediting.

Flex Plan with Trust requires 3 different actions to get maximum interest.

Then we have brokers like TigerBrokers and MooMoo, which offer MMF or money market funds, where your idle deposits are placed into short-term instruments like debt and T-bills, and in recent times, the interest rates aren’t very attractive at 1.1-1.5% for an SGD fund.

SGD and USD MMF with TigerBrokers

Chocolate Finance does a simple 2% p.a. on the first S$20k, with no requirement other than applying for an account and depositing money.

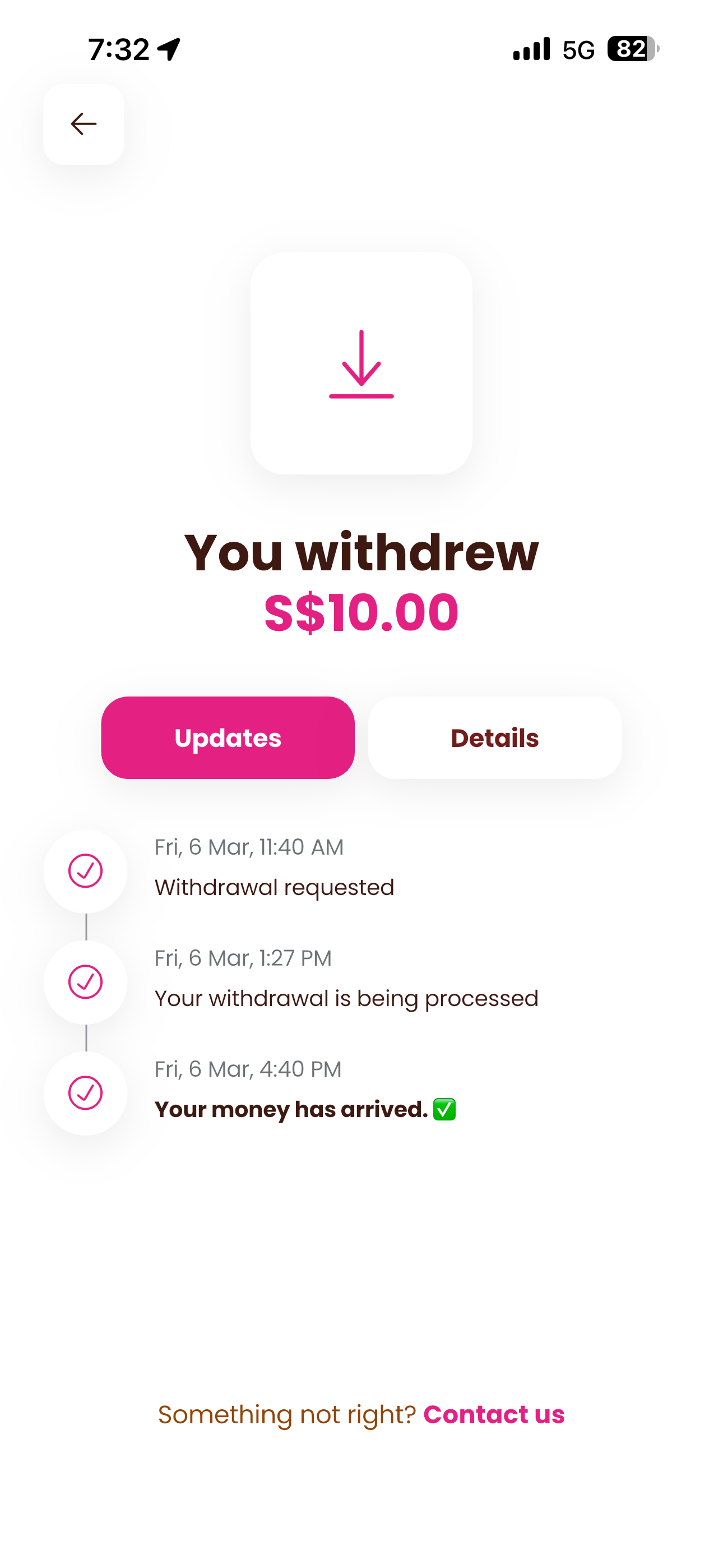

I would say the only thing you’ll have to take note of is that for withdrawals,they are not instant, although my recent withdrawal took less than 3 days, because these are financial products, which will require time to redeem the investment and transfer the money back to our bank account.

However, most withdrawals on average are completed in less than 90 hours.

So, who is Chocolate Finance for?

And I feel that Chocolate Finance is for anyone over the age of 18 who doesn’t have time to think through the criteria banks use for the highest interest. Someone who wants an above-average return with no hoops.

The way I see Chocolate Finance is as a tool/platform for me to place my idle cash, which gives me above-average returns without any hoops for me to jump through, allowing me to focus on what I do best and ensuring that I can grow my income.

Other Benefits of Chocolate Finance

But one of my favourite features of Chocolate Finance is the Visa debit card they offer. And on this channel, we have done many reviews of different cards and how they work. But something that’s really cool with the Chocolate Card is how you can earn miles while earning interest.

Chocolate Visa Debit Card

Chocolate Finance allows you to earn 2% p.a. on your first S$20k. And if you apply for a Chocolate Visa Debit Card, this allows you to spend from your account via PayWave or online purchase, like how you would with a regular Visa card.

Chocolate Finance x HeyMax Collaboration

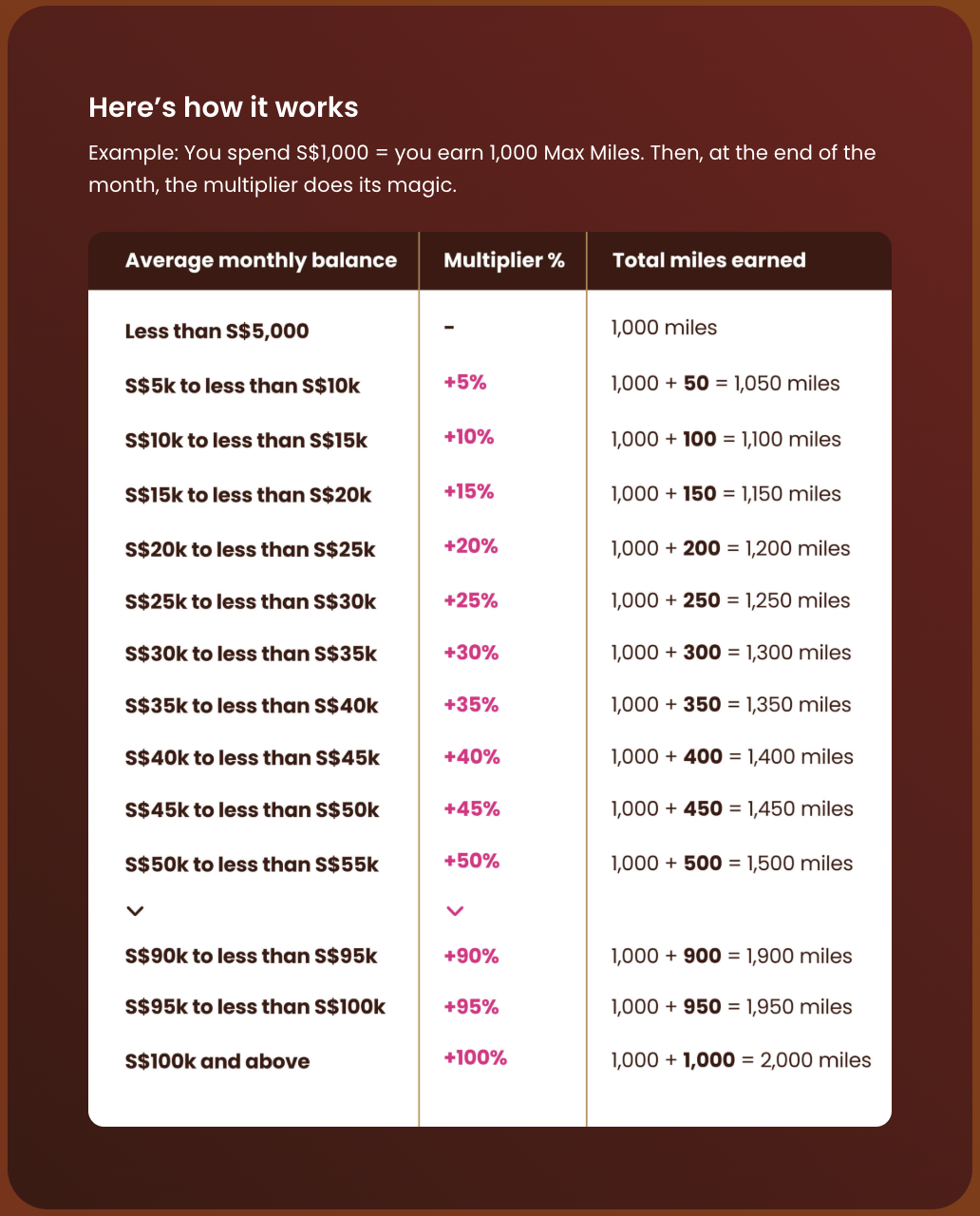

With the Chocolate Card, you’ll earn 1 Max Miles from HeyMax per S$1 spend up to the first S$1,000. And you get bonus Max Miles based on the average balance in your Chocolate Finance account.

This means, if you have S$20,000 in your account and spend S$1,000 a month, you will get 1,000 Max miles + 25% or 250 bonus Max Miles.

This is a partnership with HeyMax, where you get Max Miles on your spend, and these can be converted into supported airline miles of your choice on the HeyMax website! But this is just a bonus feature that you won’t need to use if you don’t want to.

Things to look out for

We covered all the different features and benefits that Chocolate Finance can provide. But here are some things that we need to know as well.

We cannot treat Chocolate Finance like a savings account for 2 main reasons.

Most savings accounts allow instant withdrawals, but since Chocolate Finance is an investment instrument, there is a buffer for these investments to be sold and the money to then be transferred to you. However, most withdrawals are completed in less than 30 hours.

Unlike a traditional bank, as an investment instrument, this is not covered by SDIC, but your money is safeguarded with MAS-licensed institutions.

Having said that, what keeps me really excited is that I can see the daily returns getting rolling in on a daily basis, which is really cool.

If you haven’t signed up for an account, here’s a referral link to get you started! You don’t pay anything extra, but it lets Chocolate Finance know that I was the one who sent you to them! And I hope you guys stay safe, invest safe, and see you in the next one!

Disclaimer: Chocolate Finance is a brand of Chocfin Pte Ltd and is regulated by the Monetary Authority of Singapore. The views and opinions expressed on this post are solely those of the original authors and contributors as of the date of this post and are subject to change based on market and other conditions. This is for information only and does not constitute an offer or solicitation to buy or sell any of the investments mentioned. Neither Chocfin Pte. Ltd. (“Chocfin”) nor any officer or employee of Chocfin accepts any liability whatsoever for any loss arising from any use of this post or its contents.

Please note that Chocfin does not guarantee the accuracy, relevance, timeliness, or completeness of the information provided on this post. The inclusion of any links does not necessarily imply a recommendation or endorse the views expressed within them. Chocolate’s returns are currently supported by a promotional 'Top-Up Programme', valid during the Qualifying Period and subject to terms and conditions. Past performance is not indicative of future results. All investments involve risk, including the risk of losing all of the invested amount and may not be suitable for everyone. This advertisement has not been reviewed by the Monetary Authority of Singapore.